What the 21st Century Housing Act Means for North Shore Buyers & Sellers

Real Estate News · June 2026 Congress Just Passed the Biggest Housing Bill in Two Decades. Here's What It Means for You. A plain-English breakdown of the 21st Century ROAD to Housing Act — and what it could mean for buyers, sellers, and homeowners on Massachusetts' North Shore. Home › Blog › 21st Ce

Read MoreMoving to Swampscott Massachusetts

A Relocation Guide for Young Families Life is Better at the Shore Why Swampscott, Massachusetts is one of the North Shore's best-kept secrets for families putting down roots. 📍 Swampscott, MA · Est. 1852 · Pop. ~15,500 Imagine your kids building sandcastles before school, catching the commute

Read MoreThe Ultimate Pre-Listing Checklist - Get Your North Shore Home Ready to Sell

[ { "@context": "https://schema.org", "@type": "BlogPosting", "headline": "The Ultimate Pre-Listing Checklist: Get Your North Shore Home Ready to Sell", "description": "A practical, room-by-room guide to decluttering, repairs, and curb appeal for North Shore Massachusetts home sellers — from an agen

Read MoreNavigating the Salem Real Estate Market: Pricing & Trends

Navigating the Salem Real Estate Market: Pricing & Trends What buyers and sellers in Salem, MA need to understand right now — from a REALTOR® who has worked this market for 25 years. $700K Median Sale PriceYear to Date 2026 1.6 mo. Housing Inventory Supply Multiple Offers on Hot Properties 79/100 Co

Read MoreThe Art of Timing: When Is the Golden Hour to Sell Your Home?

North Shore Market Insights The Art of Timing: When Is the Golden Hour to Sell Your Home? Twenty-five years of selling homes on the North Shore has taught me one truth: timing matters — but probably not in the way you've been told. By Jim Armstrong, Armstrong Field Group · Beverly, MA 25+ Years

Read MoreWhen to Lower Your Asking Price — And How to Avoid Needing To

Home › Blog › When to Lower Your Asking Price Seller Advice · North Shore Massachusetts When to Lower Your Asking Price — And How to Avoid Needing To The price you set on day one has more influence on your outcome than almost any other decision you'll make as a seller. Here's what happens when you g

Read MoreDon't Wait for Perfect Conditions - North Shore Real Estate Advice for the Second Half of 2026

Home › Blog › Don't Wait for Perfect Conditions Market Insights Don't Wait for Perfect Conditions North Shore Real Estate Advice for the Second Half of 2026 | Jim Armstrong, Armstrong Field Group at Aluxety Real Estate I've been selling homes on the North Shore since 2000, and one thing has been c

Read MoreJune Is National Homeownership Month — Here's What That Actually Means

North Shore Real Estate · June 2026 June Is National Homeownership Month — Here's What That Actually Means By Jim Armstrong, Armstrong Field Group at Aluxety Real Estate Every June, the National Association of REALTORS® and housing advocates across the country mark National Homeownership Month — a t

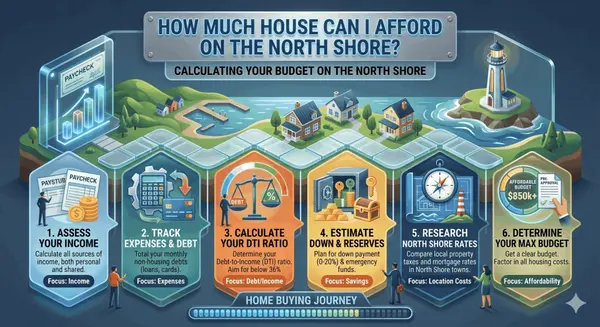

Read MoreHow Much House Can I Afford? What North Shore MA Home Buyers Need to Know.

First-Time Buyer Guide How Much House Can I Afford? What North Shore Buyers Need to Know Before They Start Looking Understanding your real budget before you fall in love with a home — a practical guide for buyers in Beverly, Salem, Danvers, and the rest of the North Shore. Jim Armstrong, REALTOR®Arm

Read MoreHow Long Does the Home Buying Process Take? | North Shore MA Guide

Buyer's Guide · North Shore Massachusetts How Long Does the Home Buying Process Actually Take? A realistic look at every stage — from your first lender call to picking up your keys — and what shapes the timeline along the way. Jim Armstrong Armstrong Field Group · Aluxety Real Estate · North Shore

Read MoreBest Home Upgrades Before Selling: Highest ROI, Biggest Wastes, and What to Do Instead

Seller's Guide · North Shore MA Best Home Upgrades Before Selling: Highest ROI, Biggest Wastes, and What to Do Instead Not every dollar you put into your home comes back at closing — and some improvements actually cost you money. Here's how to spend smart before you list.By Jim Armstrong · Armstro

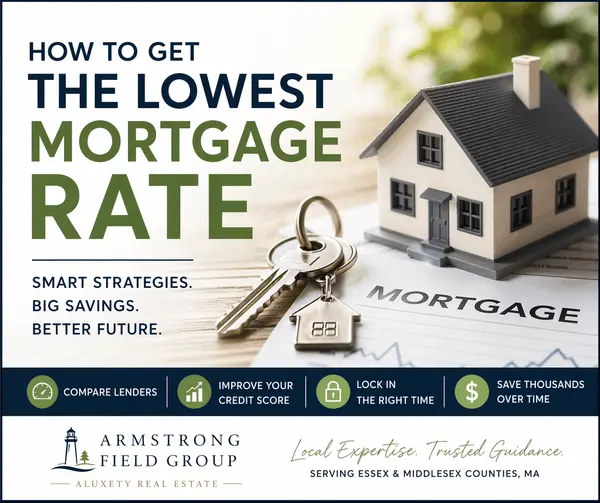

Read MoreHow to Get a Lower Mortgage Rate | North Shore MA Home Buyers

or CMS schema field ============================================================ [ { "@context": "https://schema.org", "@type": "BreadcrumbList", "itemListElement": [ { "@type": "ListItem", "position": 1, "name": "Home", "item": "https://armstrongfield.com" }, { "@type": "ListItem", "position":

Read MoreAre Home Appraisals Coming in Below Sale Price in Massachusetts? (2026 Update)

Are Home Appraisals Coming in Below Sale Price in Massachusetts? (2026 Update) If you’ve been following the Massachusetts real estate market, you’ve probably heard the question: “Are homes still appraising at the contract price?” The short answer:Sometimes—but it’s not widespread. The longer answer

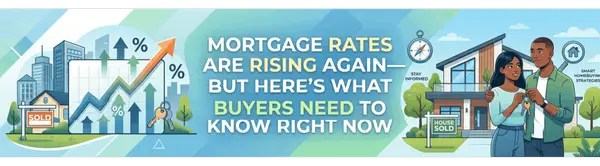

Read MoreMortgage Rates Are Rising Again—But Here’s What Buyers Need to Know Right Now

Mortgage Rates Are Rising Again—But Here’s What Buyers Need to Know Right Now After dipping below 6% not long ago, mortgage rates have started creeping back up—and naturally, that’s getting buyers a little uneasy. But here’s the bigger picture:Even with the recent uptick, today’s rates are still low

Read MorePreparing Your Beverly Home for Showings

Ready to Shine: Preparing Your Beverly Home for Showings Your decision to sell your Beverly home is a big one, and now comes the crucial stage: showcasing its best features to potential buyers. First impressions are everything in real estate, and a well-prepared home can significantly impact the off

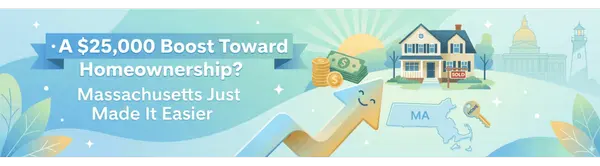

Read MoreA $25,000 Boost Toward Homeownership? Massachusetts Just Made It Easier

$25,000 in Free Down Payment Help. No Interest. No Monthly Payment.MassHousing's newest program could be the key that finally opens the door to homeownership on the North Shore.By Armstrong Field Real Estate · March 27, 2026 $25K Down payment assistance 0% Interest rate on DPA loan 135% AMI in

Read MoreDiscover Coastal Living at Beverly Landing Condos in Beverly

Discover Coastal Living at Beverly Landing Condos in Beverly If you’ve been waiting for the perfect blend of modern design, coastal lifestyle, and walkable convenience on the North Shore, Beverly Landing might be exactly what you’ve been looking for. Developed by Cummings Properties, Beverly Landing

Read MoreFinding Your Perfect Condo in Salem, MA Under $600,000

Armstrong Field Group · Aluxety Real Estate Finding Your Perfect Condo inSalem, MA Under $600,000 A practical guide to navigating one of the North Shore's most dynamic — and competitive — condo markets. Armstrong Field Group · North Shore Real Estate · Buyer's Guide Salem, Massachusetts has long

Read MoreShould You Add Onto Your Home… or Sell and Move Up?

Should You Construct an Addition… or Sell Your Home and Move Up? If you’re feeling squeezed in your current home, you’re not alone. Over the past few years, a lot of homeowners have found themselves asking the same question: “Do we expand… or do we move?” On paper, it sounds simple. In reality, it’s

Read MoreWhat NOT to Fix Before Selling Your North Shore MA Home

Home Buy Sell Blog Contact Seller's Guide · North Shore MA What Not to Fix BeforeSelling Your Home By Armstrong Field Group at Aluxety Real Estate · North Shore Massachusetts You've decided to sell. The natural instinct is to fix everything — patch every wall, update every fixture, repaint every

Read More

Categories

- All Blogs 149

- Beverly, MA 8

- Buying a Home 66

- Condos For Sale 6

- Danvers, MA 2

- Home Ownership 43

- Home Sellers Guide 13

- Homes For Sale 8

- Ipswich, MA 1

- Living on the North SHore 18

- Mortgages 10

- Prospective Real Estate Agents 1

- Real Estate Careers 9

- Real Estate Market Conditions 30

- Real Estate School 2

- Renting 1

- Salem, MA 11

- Selling a home 76

- Swampscott, MA 1

Recent Posts